China’s Water Treatment Market: Powered by Policy

China’s water treatment sector has grown into a trillion-yuan industry, reaching RMB 1.1 trillion in 2024 with a 17.7% annual growth rate. This rapid development is underpinned by strong government policy. Initiatives such as the “Water Ten Plan” and “Dual Carbon” goals integrate water governance into national strategy, creating a powerful engine for growth.

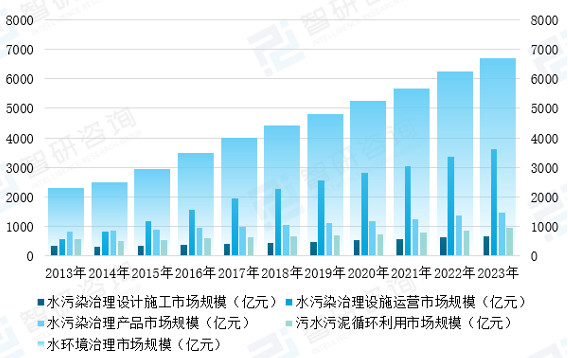

Fig.1 China's Water Environmental Governance Market Size and Sub-segments, 2013-2023

The government’s role goes beyond setting goals. More than RMB 26 billion in 2024 was allocated to water pollution control. Revised standards for pollutant discharge and expanded regulation are pushing the adoption of advanced technologies like MBR membranes and reverse osmosis. Public-private partnerships, emissions permits, and environmental taxes are phasing out outdated capacity and opening high-quality market space.

At the heart of this policy-driven model are clear, quantifiable targets. By 2025, China aims for 35% urban reclaimed water use and over 60% rural wastewater coverage. Region-specific policies—for example, the Yellow River “Waste Cleanup” campaign—create demand for customized, high-performance technologies. Meanwhile, government support for domestic innovation is helping local enterprises to compete in traditionally import-dominated segments.

From Strategy to Innovation: The China Model

China’s approach differs from Western countries by blending top-down strategy with market mechanisms. While the EU emphasizes watershed restoration and the US focuses on point-source control, China aligns national policy, financial tools, and industrial mandates. This creates a robust framework that encourages technological breakthroughs in areas like low-carbon treatment and membrane localization.

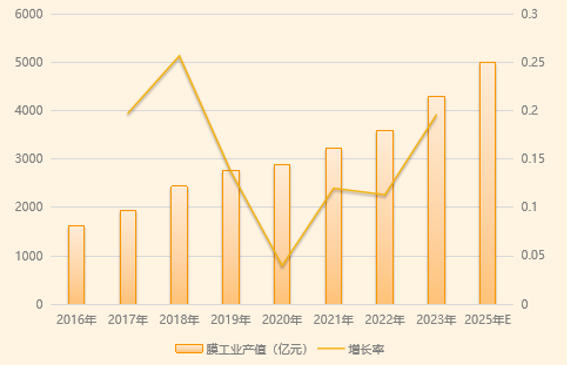

Fig.3 China's Membrane Industry Output Value and Growth Trend, 2016–2025 (100 million yuan, %)

Policy serves not only as guidance but also as a catalyst for innovation. Through coordinated use of subsidies, R&D funding, emissions trading, and mandatory equipment standards, China has built a complete “goal-tool-technology-market” loop. As a result, energy-efficient systems, smart monitoring solutions, and localized treatment units are now standard in new infrastructure projects. These technologies are also more affordable and deliverable than ever, giving Chinese products global competitive strength.

Technological Trends and Regional Opportunities

China’s geography and development gradients create diverse technology demand across regions. Eastern provinces lead in high-end adoption. Projects in Shanghai and the Greater Bay Area prioritize nutrient removal, MBR integration, and smart pipeline management. Central and western provinces focus on industrial wastewater challenges, especially in coal chemicals and metallurgy. Northeast regions work on upgrading aging infrastructure, while southwest regions target decentralized rural treatment and ecological conservation.

Across the country, technical priorities are shifting. Municipal systems are undergoing upgrades to meet quasi-Class IV discharge standards, driving the use of advanced oxidation and AI-driven control systems. Industrial zones face tightening requirements, boosting demand for membrane separation, salt-tolerant materials, and VOCs treatment. In rural and emerging markets, the push for decentralized, low-maintenance solutions is supporting modular equipment, IoT monitoring, and PFAS removal technologies.

These differentiated demands are creating vibrant sub-markets. Supported by national demonstration zones and regional incentive programs, new solutions are being tested, validated, and scaled more rapidly than ever.

China is not only transforming its domestic water treatment sector but also reshaping the global landscape of water technology. With growing exports of membrane systems, zero-discharge equipment, and turnkey solutions, Chinese enterprises are expanding their footprint across Belt and Road countries and beyond. Overseas production facilities and integrated EPC capabilities are enabling faster project delivery and stronger local adaptation. What makes China’s model distinctive is its integration of strategic planning, technical innovation, and capital leverage. This approach is now being referenced by emerging economies as a framework for sustainable water development. As new technologies continue to emerge and scale, China is poised to lead not just through manufacturing strength, but through a replicable model of policy-driven innovation with global relevance.